Well, the day is finally here… I’m officially the big 3-0! If you’ve read my site at all over the course of the last 5 or 6 years, you might know that it’s been a longstanding goal of mine to pay off my student loans by the time that I turn 30.

So did I do it?!

Unfortunately, no. I’ve known for a while that it probably wasn’t going to happen by my birthday, but I was holding out hope for a Hail Mary pass at the very last minute. That play didn’t happen and I still have a pretty sizable balance.

Let’s take a look back at what I have accomplished, though. I’m pretty bummed about it and find methodical analysis of my finances almost as soothing as a nice, full-bodied glass of red wine.

Where My Student Loans Started

I made my first student loan payment in May 2011. I’ve been making payments on my student loans for exactly 6 years! My how time flies! However, I didn’t enter full repayment in May 2011, as I was still in grad school. Arcane rules for one of my private student loans required me to start making payments on my loan no longer than X years (I can’t remember how many) after I took the loan out, even if I was still in school. I made the first payment for (almost) the rest of my student loans in December 2011. I made the first payment for the last loan in April 2012. When I started paying off my student loans:

- After capitalization of my student loans (interest earned in deferment is added to the principal), I owed just over $96,000.

- My minimum balance was $756.07.

- I had 15 separate loans split across 3 different servicers. This meant that my minimum balance was split across 3 different checks.

- I had 3 private loans, 1 Perkins loan, and 11 Federal loans.

- I decided to use a graduated repayment plan for 2 of my federal student loans from graduate school. A graduated plan means that the loan will still be paid off in 10 years, just like a standard repayment plan; however, the minimums start smaller and increase in size every 2 years.

Thankfully, I was able to get a full time job shortly after graduating from graduate school. I was then able to segue my education and job into a more lucrative (and personally fulfilling!) career that has resulted in me earning much more than I ever would have as a librarian.

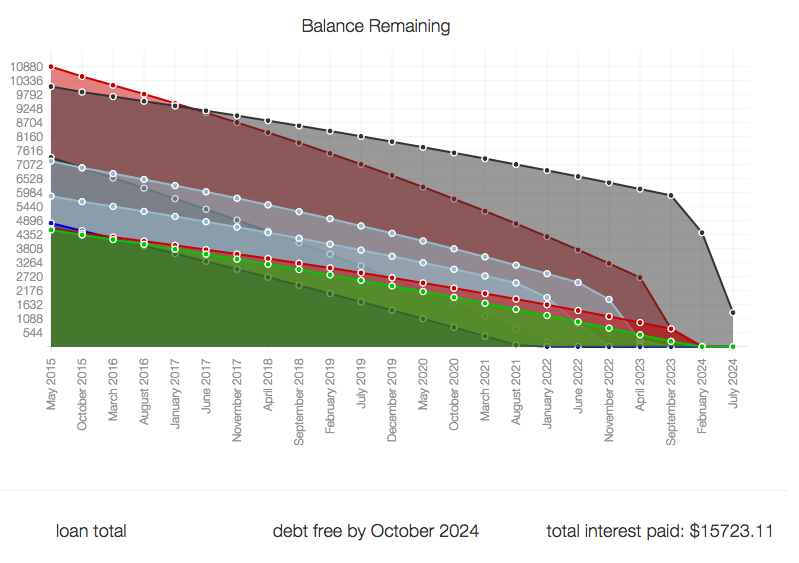

Where My Student Loans Are Now

Even though I started with a LOT of student loans, over the course of the last 6 years (and really 5.5 if you’re counting when the majority of my student loans went into repayment), I’ve been able to get a fairly big handle on my student loans:

- My student loans balance is hovering around $25,000. I’ve paid off 75% of my original balance!

- My minimum balance is ~$440. Although I’ve paid off a number of my individual loans, my minimum balance has not gone down substantially, since my graduated repayment loans’ minimum balance has increased.

- I have 4 remaining loans. I’ve paid 11 loans in full.

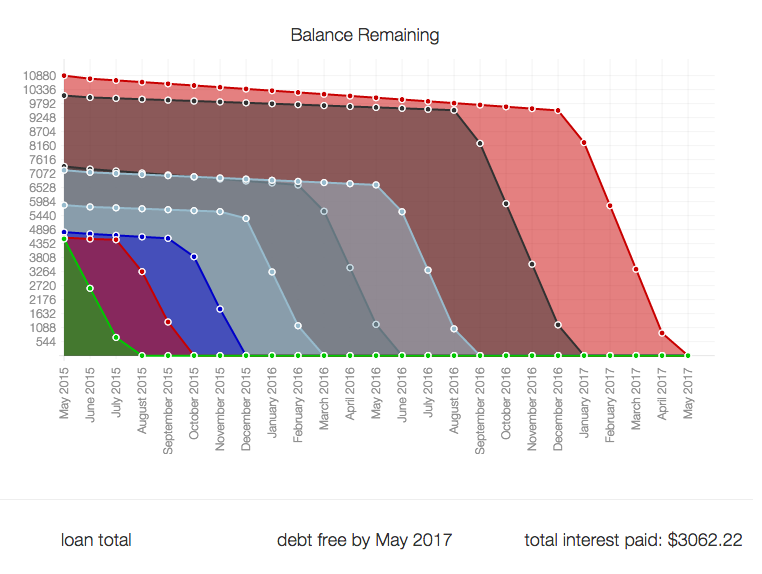

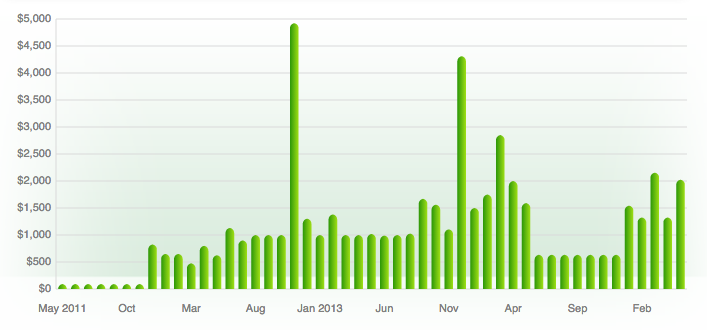

As you can see from the chart below, the bulk of my spending on student loans has been between 2012 and 2016. I’ve held steady at paying $20,000 in student loans for each of the last two years. This year, I hope to pay the rest off. I expect that interest will result in me contributing up to $26,000 to finish the loans off.

When you add up all of my payments, I’ve contributed over $91,000 to my student loans! A quick calculation tells me that if I end up contributing $117,000 ($91,000 to date plus my remaining balances), then I’ll have spent $21,000 on interest. Lord, the things I would do with $21,000!!! Or even, Lord, the things I would do with an extra $117,000 if I hadn’t had student loans in the first place.

How I Plan to Pay Off My Student Loans

Clearly, I’ve made a ton of progress; however, I still have a long way to go. In fact, I’ve been paying my loans for 5.5 years and my balance is now only getting to what the U.S. national student loan balance average is. That’s pretty sobering, if you ask me.

My goal is to pay the rest of my student loans by the end of the year. This year has been a bit crazy for us when it comes to finances. We got married (and paid for our wedding) and we also moved to Germany. The wedding cost a bit (although we were under substantially under the national average for that!) and moving will end up costing us quite a bit with furniture costs and security deposits. Stella’s final months were also quite expensive.

In the hubbub of moving, we’ve acquired quite a bit of cash. We sold our cars, received our security deposit back, had been earning steady incomes (and trying our best to not spend money on anything that didn’t contribute to the move), received wedding gifts, and sold some of our furniture.

We’d like to use a lot of that cash to make a big dent in the student loans. But first, we need to do a couple of things:

- Pay security deposit for our new apartment

- Purchase furniture and other household items

- Max out ROTH IRAs for 2017 (doubles as a 3-month emergency fund)

- Maintain a cash 3-month emergency fund

We’ll put whatever is left towards a large chunk of the loans. We are planning to rent an apartment that will allow us to save about 500€ per month towards retirement and other long term savings. Since we will have done all of our planned retirement savings for the year, that money will go towards the student loans until they are paid off.